Listen to the article

Listen to the article

Picture this: fixed income investments. They might seem a bit boring next to the exciting stock market or the latest crypto coin, but trust me, they’re key to keeping your money safe and growing.

So, why are we chatting about this in 2024? Well, this year’s looking pretty wild with all its ups and downs. Fixed income investments are like lending your money out and getting it back with a little extra.

Think of bonds or savings accounts. They’re super important for ensuring you have a well-balanced money plan, especially when the market’s doing the tango.

These investments are the calm in the storm, giving you a steady cash flow when other things might not. And when we stack them up against fancier options that promise big returns (but with big risks), think of fixed incomes like your reliable car. It gets you from A to B safely, while those riskier bets are more like flashy sports cars – exciting, but you might end up paying more for that thrill.

What are Fixed-Income Securities?

Fixed-income securities are a way for investors to lend money to companies, which they use to finance projects or keep their operations running. In return for your investment, you receive a set amount of interest, usually given out as coupon payments. These payments are made every six months, and when the investment period ends, you get back the initial money you put in.

What are the Types of Fixed Income Investment opportunities available?

The world of Fixed Income investments has changed a lot. In the past, options were mostly limited to Bank Fixed Deposits, the Public Provident Fund, and National Savings Certificates.

Nowadays, there’s a broader range of choices within the Fixed-Income category. This includes treasury bonds, corporate bonds, and debt mutual funds. These new choices can give you higher returns than the old ones and are generally less risky than investing in stocks.

Here’s a brief overview of the popular fixed income investment opportunities in India:

Bank Fixed Deposits

- Yield: The yield on bank fixed deposits in India varies depending on the bank and the tenure of the deposit. As of the latest data, the yield on bank fixed deposits ranges from around 5% to 7% per annum.

- Maturity: The maturity period for bank fixed deposits can range from as short as 7 days to as long as 10 years, depending on the investor’s preference.

- Credit Risk: Bank fixed deposits are considered relatively safe investments as they are backed by the Deposit Insurance and Credit Guarantee Corporation (DICGC) for up to Rs. 5 lakhs per depositor per bank.

Real estate structured debt

- Yield: Real estate-backed investments have the potential to deliver appealing returns through interest payments and potential capital appreciation. Investors can generally expect yields to range from around 8% to 12% per annum.

- This relatively high yield reflects the increased risk associated with real estate investments compared to more traditional fixed-income securities.

- Maturity: Real estate structured debt offers a range of maturity periods, typically from 2 to 5 years. This shorter to medium-term duration caters to investors looking for opportunities beyond the very short term but without the long-term commitment required by other types of real estate investments.

- Credit Risk: This financial product presents fixed-income prospects by using real estate assets as collateral, thus carrying a low risk. Nevertheless, it’s crucial to bear in mind that returns may vary depending on market conditions and the performance of the underlying assets.

Public Provident Fund (PPF)

- Yield: The current yield on the Public Provident Fund (PPF) in India is around 7.1% per annum.

- Maturity: The maturity period for a PPF account is 15 years, which can be extended in blocks of 5 years.

- Credit Risk: PPF is a government-backed savings scheme, making it a low-risk investment option with a sovereign guarantee.

National Savings Certificates (NSC)

- Yield: The current yield on National Savings Certificates (NSC) in India is around 6.8% per annum.

- Maturity: The maturity period for NSC is 5 years.

- Credit Risk: NSC is a government-backed savings instrument, ensuring capital protection and low credit risk.

Treasury Bonds

- Yield: The yield on Indian treasury bonds varies based on the tenure and prevailing market conditions. As of the latest data, the yield on treasury bonds ranges from around 6% to 7%.

- Maturity: Treasury bonds have varying maturities, ranging from short-term (less than 1 year) to long-term (up to 30 years).

- Credit Risk: Indian treasury bonds are considered low-risk investments as the government of India backs them.

Corporate Bonds

- Yield: The yield on corporate bonds in India varies depending on the issuing company, credit rating, and tenure. As of the latest data, the yield on corporate bonds ranges from around 7% to 9%.

- Maturity: Corporate bonds have varying maturities, typically ranging from 1 year to 10 years.

- Credit Risk: Corporate bonds carry credit risk based on the issuing company’s financial health and credit rating.

Debt Mutual Funds

- Yield: The yield on debt mutual funds in India varies based on the underlying securities and market conditions. As of the latest data, the yield on debt mutual funds ranges from around 6% to 8%.

- Maturity: Debt mutual funds do not have a fixed maturity date as they invest in a portfolio of fixed-income securities with varying maturities.

- Credit Risk: Debt mutual funds carry credit risk based on the quality of the underlying bonds in their portfolio. Professional fund managers manage this risk.

Why are Fixed Income Investments a portfolio essential?

You might wonder why there’s always so much buzz around adding fixed income investments to your portfolio. Well, there’s plenty of good reasons, and here’s the rundown:

- Diversification: Ever heard the saying, “Don’t put all your eggs in one basket”? That’s where diversification comes into play. By mixing in some fixed income investments like bonds, CDs, and money-market funds into your portfolio, you’re essentially spreading your risk.

- These types of investments usually don’t move in the same direction as stocks, so your portfolio might keep its cool when the stock market is having a roller-coaster day. It’s like having a safety net that helps keep things stable when things get shaky.

- Consistent Income: Who doesn’t like a steady paycheck? That’s what fixed-income investments can offer. Through interest or dividends, you get a regular flow of cash. This is perfect if you’re looking for a way to earn money on the side without dipping into your principal amount. It’s like having a reliable tenant who pays rent on time, every time, helping you cover expenses or save up for something big.

- Risk Mitigation: Let’s face it: investing always comes with its share of risks. However, fixed-income investments are generally seen as the safer bet compared to stocks. They’re the tortoise in the race; they might not get you rich overnight, but they offer a level of stability and peace of mind, especially if you’re not in the mood for a financial roller coaster ride.

- Preservation of Capital: The main goal of fixed income investments is to keep your initial investment safe and sound, bouncing back to you in full when the time comes. This is great if you’re not too keen on the idea of your hard-earned money taking a hit because of market ups and downs. It’s about protecting what you’ve got while making something extra on the side.

- Hedging Against Inflation and Interest Rate Risks: Now, this is where it gets a bit technical. Some fixed income investments, like those fancy floating-rate and inflation-linked bonds, can be your shield against inflation eating away at your buying power. And then there’s interest rate risk – the nemesis of bond prices. But with the right strategy, you can manage this risk and keep your investments on track.

Alternative Real Estate Investments as Fixed Income Options

Broadening the horizon beyond traditional fixed-income securities, alternative real estate investments emerge as an intriguing choice. These typically manifest as Real Estate Investment Trusts (REITs) or direct ownership in income-generating properties, offering tangible assets that can yield rental revenue over time.

They’re noteworthy for their potential to yield higher returns compared to traditional securities, along with the added benefit of property appreciation.

How To Incorporate Fixed Income and Alternative Real Estate Investments into Your Portfolio?

How should you blend these types of investments into your portfolio? A diversified strategy is key. By dedicating a portion of your portfolio to fixed-income securities, you counterbalance the inherently higher risks of equities.

Alternative real estate investments can be introduced as part of your fixed income allocation or as a distinct real asset category tailored to your risk tolerance, investment timeline, and income needs.

Fixed Income vs. Alternative Investments

| Feature | Fixed Income Investments | Alternative Investments |

| Definition | Investments in securities that pay regular interest and return the principal at maturity. Examples include bonds and CDs. | Investments outside of the traditional stock, bond, or cash categories, including private equity, real estate, and commodities. |

| Risk Level | Generally considered lower risk, especially with government and high-grade corporate bonds. | It can vary widely but often higher risk due to less regulation, lower liquidity, and more complex strategies. |

| Return Potential | Typically, they offer lower return potential in exchange for lower risk. | Potentially higher returns compared to traditional investments, compensating for the higher risk. |

| Liquidity | Usually, it is more liquid, especially for government and corporate bonds. | Often less liquid, with some investments requiring longer holding periods to realize returns. |

| Income Generation | Primarily focused on generating regular income through interest payments. | It may not focus on income generation; returns are often realized through capital gains at the end of the investment period. |

| Tax Considerations | Interest income is usually taxable, although some government securities may be exempt from state and local taxes. | Tax treatment can be complex and varies by investment type; some may offer tax benefits or deferrals. |

| Suitability | Suitable for conservative investors seeking predictable returns and preservation of capital. | More suited for sophisticated investors willing to take on higher risks for the possibility of higher returns. |

Looking Ahead: The Role of Fixed Income Investments in 2024 and Beyond

Fixed-income and alternative real estate investments will become increasingly significant in the coming years.

With the economic recovery expected to unfold gradually, the stability brought by these asset classes might be precisely what you need to navigate the evolving landscape. Emerging trends like sustainable investing and digitising real estate assets could also reshape the investing environment, offering new prospects within the fixed-income domain.

Bottom Line

The simplest strategy is to spread your funds across different asset types to attain stability in your investments while also generating income.

Before setting your asset allocation, it’s crucial to keep these points in mind:

- How much risk are you willing to take?

- What are your liquidity needs?

- How much market fluctuation can you withstand?

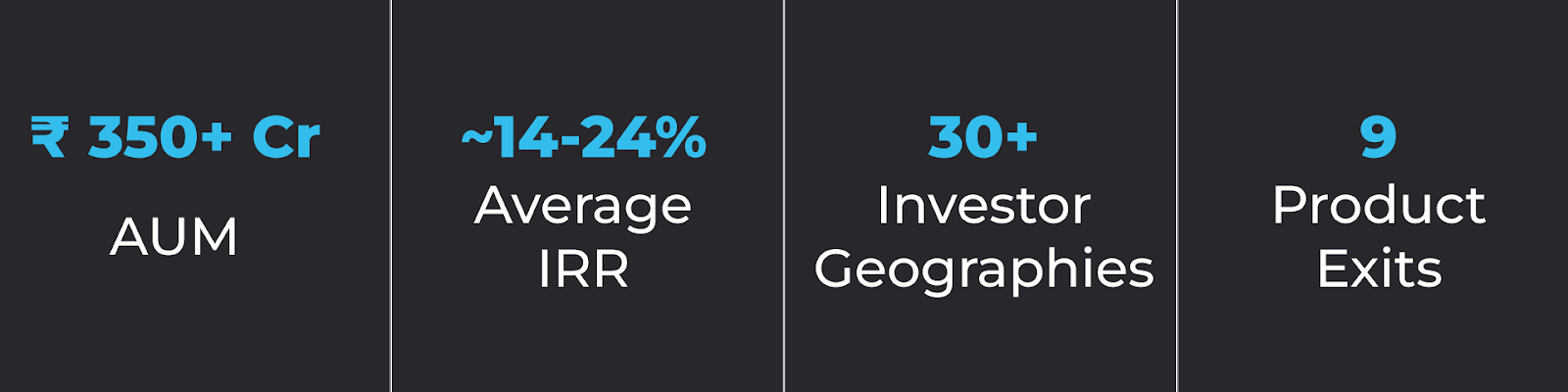

Assetmonk is a pioneer in alternative real estate investment, and we understand the immense potential in the Indian commercial real estate industry. We make alternative assets, such as real estate, more accessible.

We have customised investment options to suit individual financial goals like passive income capital appreciation and portfolio diversification.

Our expertise is identifying opportunities with high yields within the retail, office, and industrial asset classes. This enables our investors to maximize profits while diversifying their portfolios.

We offer various alternative investment options, such as fractional or joint ownership of high-end commercial properties, sub-leasing ventures, etc. Trophy locations with the potential for high Internal Rates of Return (IRR) are prioritized, and due diligence is done to ensure these provide profitable returns for our investors.